Shine the Light on your Cash

YOUR Cash Matters - Make it work for you.

Individuals, Businesses, Charities, Power of Attorneys, Trusts, Clubs and Associations

A Personal and Friendly Service

delivered with Precision, Skill and Expertise

Paul Alkins

Founder and creator of The Savings Bureau, with 26 years of experience in Regulated Financial Planning and 8 years as a Director of a National IFA.

He left this role to set up Deposit Sense Ltd and has spent the last 16 years showing Financial Advisers how they should help their clients to Maximise and Protect the Value of their Cash as part of the Financial Planning Process.

Recognising that Financial Advisers do not cover all clients, he has now set up The Savings Bureau to ensure that everyone, including those that do not wish to work with a Financial Adviser, has the opportunity to Maximise and Protect the Value of their Cash.

Lisa Alkins

Lisa was one of the longest serving staff members at Reaseheath College when she left after 27 successful years.

Starting as a Lecturer in the Animal Science and Behaviour Department, teaching the scince and genetics of animals, she progressed into the Trainging and Development Department to ensure consistent lecturing delivery standards were developed across the Collgeg, for the benefit of all students.

She is now looking forward to applying her skills to help others achieve new standards and reqards from the effective management of their cash.

Take Control of your Cash

Without Cash, nothing is possible.

This is why, Maximising and Protecting the Value of your Cash, should also be the most fundamental and essential 'activity' we undertake when managing your finances.

Before you do anything else, Maximise and Protect the Value of your Cash.

Zero Risk and only Positive Upside!

Use the tools on this website to Value your Cash and see how much more you could be making by managing it effectively.

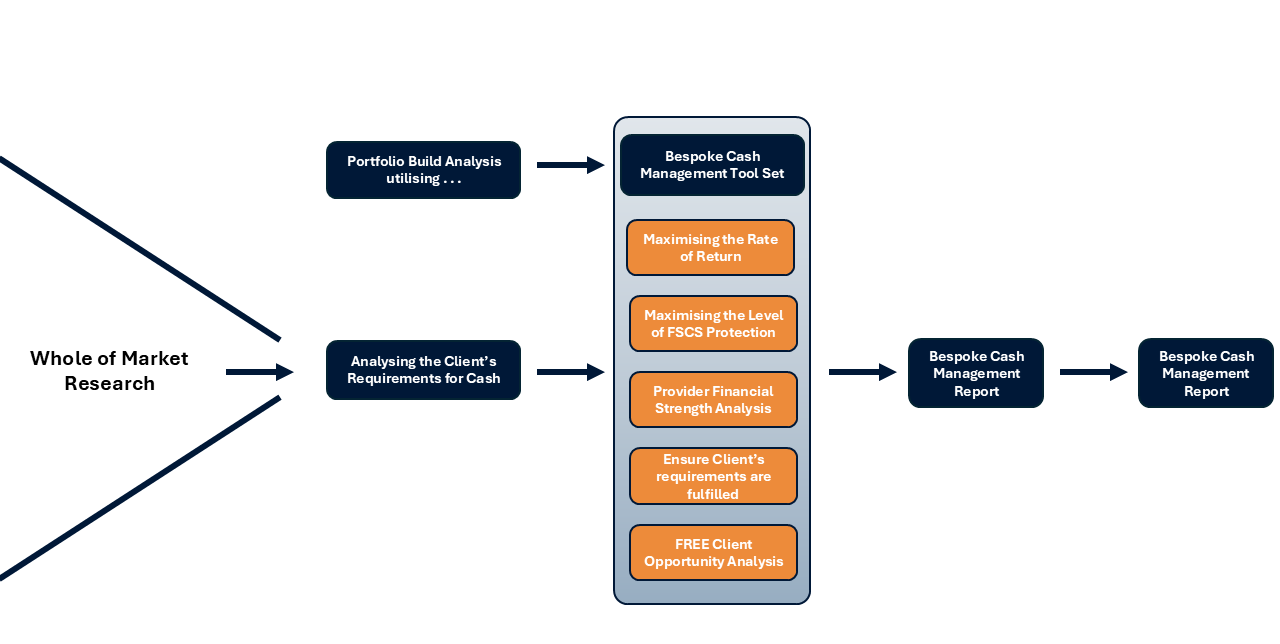

What We Do . . .

- Identify the Best Accounts that pay the highest rate of interest

- Make sure that FSCS protection is not lost by ensuring there is no duplication of Banks or Building Societies

- Analyse the Financial Strength Rating of each Bank or Building Society for added protection

- Review the results against the Client's requirements to make sure they have been met

- Show the Opportunity Value to the Client to see if they want to proceed

Our Process

- Whole of UK Market Research - We research the whole of the UK market to find the best rates and highest levels of FSCS protection for your cash.

- Financial Strength Analysis - We analyse the financial strength of banks and building societies to ensure your cash is placed with secure institutions.

- Tailored Cash Management Plans - We create personalised cash management plans that align with your financial goals and risk tolerance.

- Portfolio Generation - We generate a diversified portfolio across multiple banks and building societies to maximise returns and minimise risk.

- Ongoing Monitoring and Adjustments - We continuously monitor your cash portfolio and make adjustments as needed to ensure optimal performance.

- Expert Support and Guidance - Our team of experts is always available to provide support and guidance on your cash management strategy.

How we have Helped

The gentleman had £248,000 and his wife had £298,000 held on deposit with around 80% of it in Cash ISAs for tax efficient growth.

They had been managing their cash themselves and they had 15 different accounts, which equated to an average of just over £36,000 in each account.

They were earning around £12,500 annual interest.

9 of the 15 accounts were accessible and I showed the clients how to reduce the number of accounts down to 3 and how to increase the interest rate return to over £18,000.

We will be managing the remaining accounts when they mature and the money becomes accessible. When the time is right, this will reduce the number of accounts down to 5 in total (down from 15) and the interest rate return will be around £22,000.

This gentleman had £30,000 in a 'Premier' Account provided by Lloyds Bank. The Account came with additional benefits for a monthly fee of £21.00.

Upon reviewing the benefits offered, the monthly cost of the account and the interest rate paid, the client realised that it was much better to move the money into Cash ISA accounts, paying £0 tax, with a better interest rate return.

Naturally, only £20,000 can be placed in the current tax year and the balance will be sorted out in the new 2026 tax year after 6th April.

The new interest rate return will be over £1,250. which is much more compensation than was previously obtained from the Premier Account with the added costs and benefits.

This lady had £146,000 with Barclays Bank and the Post Office. She was convinced she was getting a good rate of interest and was shocked when she saw she was eaning less than £400.

However, she was extremely pleased when we showed her how to get in excess of £5,000.

Less than £1,000 interest to over £24,000

This gentleman was earning less than £1,000 interest on the £800,000 he held with HSBC, with only £85,000 protected by the FSCS.

Following our rules of engagement the interest rate return increased to over £24,000, and the FSCS protection increased to 100%.

'37' Accounts earning £7,500 interest to 7 Accounts earning over £32,000

This lady was managing her own money and had accumulating 37 different savings accounts with just over £637,000 deposited in them. She had 100% FSCS protection and she thought she was doing well by earning just over £7,500 interest.

She was ecstatic when we showed her how to reduce the number of accounts down to 7 and increase the interest she was earning to over £32,000.